The following is a guest blog post:

Altria has caught the eye of value, dividend investors. Altria shares have dropped over 30% since their highs in 2017 and the dividend is now yielding over 6%. Let’s look into the business and see if this high-yield is sustainable.

Altria Sales and Business Growth

Altria is one of the world’s largest tobacco companies. Its market cap is around $100 billion and the business generated close to $20 billion in sales last year (after excise tax). The tobacco industry is regulated and the government takes a good chunk of the sales.

Tobacco is an addictive product so customers tend to stick around. This give Altria strong pricing power. If the government increases cigarette taxes, the increase is passed along to customers. This pricing power has helped Altria grow its sales steadily over the last five years.

The company is also growing through acquisition. Altria acquired a 35% stake in JUUL for about $13 billion. JUUL is an e-cigarette company that sells non-combustible products. This is a solid move for Altria as the percentage of traditional cigarette smokers is declining. Although, JUUL’s fast growth has caught the eye of government regulators.

Cannabis is another area Altria has expanding into. The company bought a 45% stake in Cronos and has warrants to bump the ownership up to 55% over the next four years. Cronos is a top Canadian marijuana company. The market potential is huge and full legalization in the U.S. could unlock billions in sales for the growing company. Altria is a sound business with a strong management that’s forward looking.

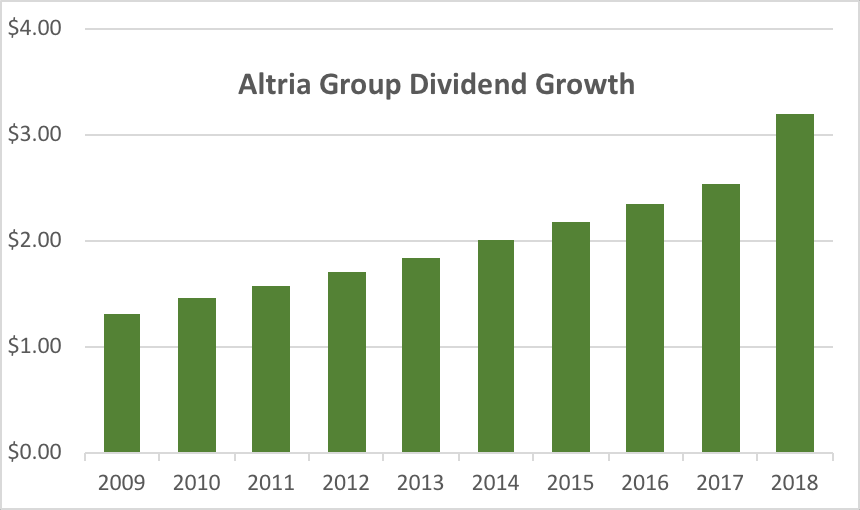

Is Altria’s High-Yield Dividend Safe?

Altria’s board of directors has increased the dividend since 2009. It’s climbed from $1.32 per share to $3.20. That’s huge growth for dividend investors… although, is Altria’s dividend safe?

The percentage of smokers is declining but Altria’s strong pricing power supports the high-yield dividend. The company is also positioning itself for a new future. Adding e-cigarette and cannabis sales to Altria should produce growing cashflows over the next decade.

The company is investing its cash flow well and rewarding shareholders. Altria has grown its dividend per share rapidly but it hasn’t had to increase its total dividend payout as much. The company has been buying back its own shares. Total Altria shares outstanding has dropped from 2.1 billion to below 1.9 billion.

Another key factor in determining Altria’s dividend safety is the debt load. Altria has $25 billion in total debt but it’s spaced out well. Altria has more than enough projected cash flow to pay it off and continue paying its high-yield dividend.

Overall, Altria is a better bet than most dividend stocks at current valuations. There are risks (mainly regulatory uncertainty) but the risk-to-reward is solid. DivHut recently bought into MO at great price and is set to collect the high dividend yield going forward.

Hut/Guest writer –

Altria is great – how is the payout ratio and operating cash flow coverage looking? That could play a big part for potential/additional investment.

-Lanny

Hi DD,

I’d call MO’s payout ratio moderate and still well covered for that juicy yield.

Mo is definitely appealing at current prices and love the moves with juul and chronos.

Dope will be huge and mo has the expertise and financial backing to excel in this upcoming sector.

cheers.

Passivecanadianincome recently posted…Dripping The Pipes – Oh Yeah!

Hi Passivecanadianincome,

Vaping and cannabis are the future trends. They way states are voting regarding cannabis I could see it becoming legal on a federal level. Might as well take advantage of that potential growth to offset the traditional smoking losses. MO under $60 still looks good to me.

Dividend growth has been really fast for the past decade and the current +6 % yield is looking really attractive too! I think it’s a smart move to start focusing on e-cigarette and cannabis as the percentage of smokers will probably continue to decline.

Dividend Deluge recently posted…Recent Buy – Mintos P2P loans

Hi DD,

Totally agree with your comment. I don’t expect MO to be a huge dividend grower for the foreseeable future but that is offset by the juicy current yield you are getting for simply holding.