The following is a sponsored post:

World Fuel Services is a great dividend paying stock. They are a leading global fuel services company principally engaged in fuel distribution to airports & airlines, retail fuel stations, seaborne shipping companies, NATO, & U.S. & foreign governments. They have some others, but these are currently their core businesses.

The company went public in 1984 as International Recovery Corporation and subsequently acquired Trans-Tec in 1995. Along with Trans Tec came its two founders, Paul Stebbins and Michael Kasbar. Paul Stebbins then served as CEO from 2002 to 2012 and Michael Kasbar subsequently took over as CEO in 2012 and is still the CEO as of today.

Under Paul Stebbins tenure, World Fuel Services grew revenue and earnings from $1.4 billion and $17 million in 2002, to almost $35 billion and $194 million by the time he left in early 2012. This equated to a compounded growth rate of earnings of almost 31%. World Fuel Services was then featured in fortune magazine under the headline “The only fortune 500 company that’s grown faster than Apple”1. What has happened since then? Has World Fuel Services continued to compounded earnings at high growth rates?

Given only the information above, you would have been inclined to say it will probably compound earnings at a high growth rate. Unfortunately, the outcome was the opposite, and over the next 6 years, pre-tax adjusted earnings has gone from $238 million in 2011, to $147.1 million2 in 2017. This equates to a compounded loss of earnings of 7.7% per year. So, what happened?

To answer this question, we need to understand the economics of the business – so let’s get started. World Fuel Services relies on three main factors which determine the earnings of their three segments:

1. Underwriting fees from hedging oil prices and delivery dates for clients

The period since the collapse of oil prices has been less volatile than previous periods such as from 2007 to 2010. This has led to a decrease in the quantity of hedging contracts demand by their customers.

2. Spread between the purchase price of processed petroleum products3 and the sale price to customers

It is hard to increase the spread as this is a competitive market and unusually large profits would invite more competitors to enter. This would decrease the spreads as competitors would undercut each other. In addition, NATO and government customers are more profitable, so they offer a higher spread than private enterprise.

3. Volume of fuel sold

Volume sold increases due to either increased use of fuel by World Fuel Services’ current clients and/or market share gains against their competitors.

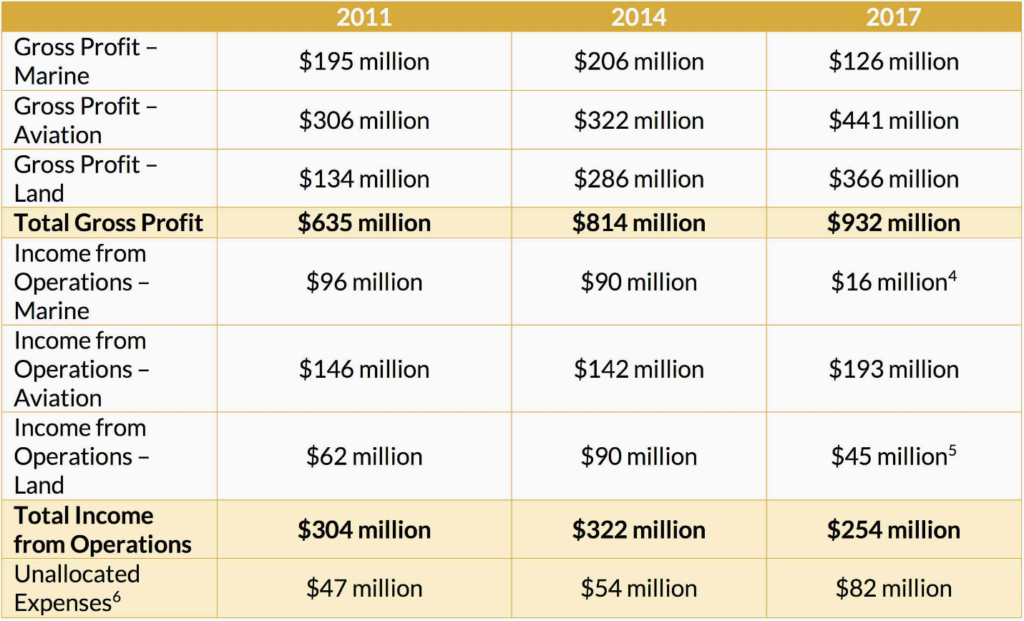

We conclude that volume of fuels sold, the spread (including the customer base), and the fees earned on hedging some of these contracts are the main drivers of World Fuel Services’ earnings. This minus the operating costs gives us the money the company makes before interest and taxes. Therefore, it is critical that they have a good handle on their costs. The table below provides snapshot of some important figures:

Clearly, the marine and land segments are struggling while the aviation segment is thriving. The rise in unallocated expenses is notable as well as financing costs which are not included but totaled $61 million in 2017. What happened over that time to cause such negative results?

Read the full analysis on emperorinvests.com.

1 – http://fortune.com/2013/05/20/the-only-fortune-500-company-thats-grown-faster-than-apple/

2 – Note: This is adjusted for goodwill and restructuring charges as well as excess financing charges. These adjustments require a lot of judgement on the part of the analyst to discern whether there will be further charges that will require a cash outlay from the business or not. These charges reflect the fact that money that could have been returned to shareholders as a dividend in the past has instead been reinvested in the business and those were bad investments. They are an indication of management’s capital allocation decisions and outcomes.

3 – Examples of processed petroleum products includes bunkers for ships & jet fuel for airplanes

4 – Adjusted for impairment of goodwill & restructuring charges

5 – Adjusted for restructuring charges of roughly $52 million

6 – This excludes financing costs

Forward Looking Disclosure

Certain statements that we make above may constitute “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include information concerning future strategic objectives, business prospects, anticipated savings, financial results (including expenses, earnings, liquidity, cash flow and capital expenditures), industry or market conditions, demand for and pricing of our products, acquisitions and divestitures, anticipated results of litigation and regulatory developments or general economic conditions. In addition, words such as “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “projects,” “forecasts,” and future or conditional verbs such as “will,” “may,” “could,” “should,” and “would,” as well as any other statement that necessarily depends on future events, are intended to identify forward-looking statements. Accordingly, these statements are only predictions and involve estimates, known and unknown risks, assumptions and uncertainties that could cause actual results to differ materially from those expressed in them. Forward-looking statements are not guarantees, and they involve risks, uncertainties and assumptions. Although we make such statements based on assumptions that we believe to be reasonable, there can be no assurance that actual results will not differ materially from those expressed in the forward- looking statements. Our actual results could differ materially from those anticipated in such forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs.

We caution investors not to rely unduly on any forward-looking statements and urge you to carefully consider the risks described in any filings with the Securities and Exchange Commission from time to time, including the company’s most recent Annual Report on Form 10-K and subsequent Forms 10-Q, which are available on the SEC’s website at sec.gov. We expressly disclaim any obligation to update any forward-looking statement in the event it later turns out to be inaccurate, whether as a result of new information, future events or otherwise.

1 thought on “World Fuel Services: A Dividend Stock With Higher Growth Than Apple?”